Has the resilient Australian Core Property sector now entered the Goldilocks zone?

With attractive starting valuations, above average expected rental growth, increasing transaction evidence and many institutional investors now underweight, Australian core property has now entered the investor ‘Goldilocks’ zone.

What is Australian core property?

In the world of institutional investment, ‘core’ property has long been viewed as an integral component of portfolios. In the Australian context, this asset class—comprised of high-quality, well-located commercial real estate with stable income streams—has demonstrated its resilience over many cycles.

At its heart, Australian core property refers to "institutional-grade" assets. These are typically the premium office towers in CBDs like Sydney and Melbourne, prime logistics hubs near major infrastructure, and dominant shopping malls.

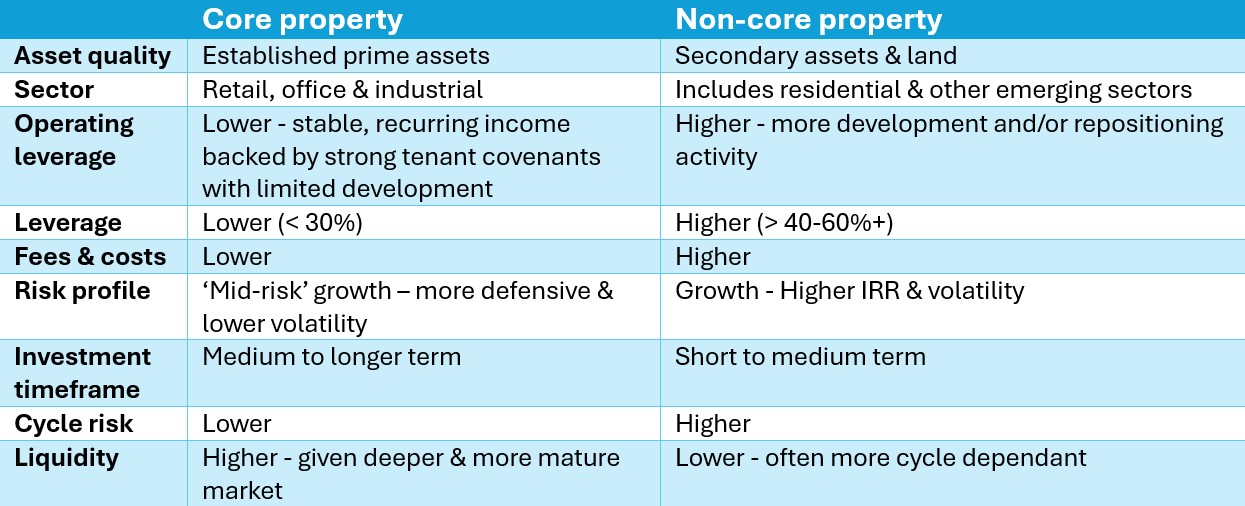

The table below illustrates typical differences between core and non-core property.

The table clearly demonstrates that the risk / return profiles of core compared to non-core strategies are fundamentally different.

Non-core: moving up the risk curve

Several factors can greatly increase the risks associated with non-core property strategies:

• Asset quality – Investing in secondary assets instead of top-tier core assets raises market risk.

• Operational leverage – Pursuing strategies like development, refurbishment, or major leasing activities adds to operational risk.

• High leverage – Relying on higher levels of debt, common in non-institutional strategies, heightens financial risk.

When one or more of these factors are present, the overall risk becomes even greater, moving the strategy into non-core territory.

The diversification trap

Many investors believe that adding “property” can diversify their portfolio.

But if the strategy becomes non-core, it becomes more cycle-dependant as it includes riskier activities such as high leverage, lower asset quality, speculative outcomes, increased operational risk such as development and short-term capital plays — then the defensive benefit of property can disappear.

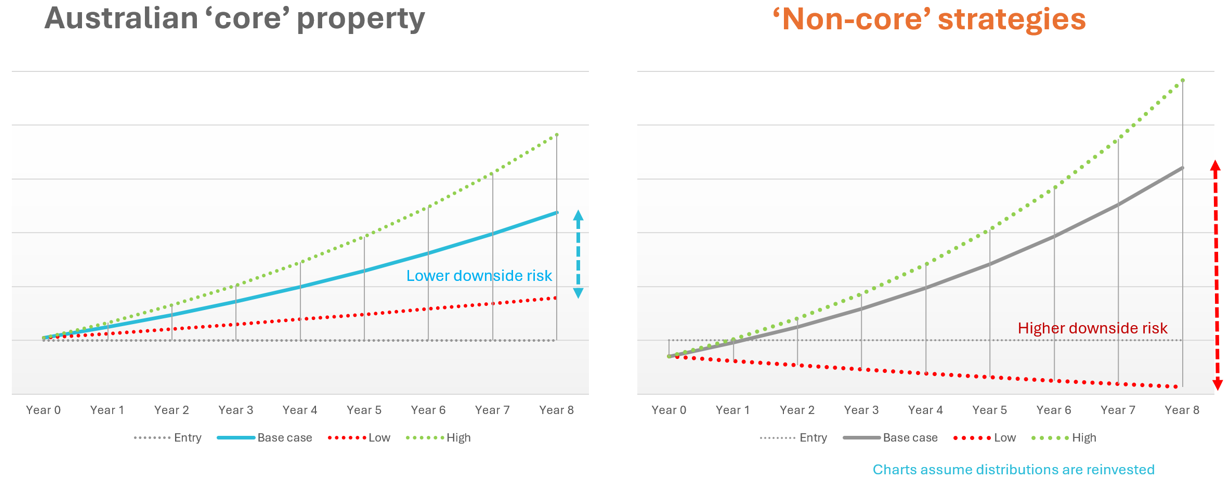

What core and non-core property returns can look like

Risk & return go hand in hand i.e. generally, higher returns require more risk, whereas lower returns have lower risk. As illustrated below, core property should deliver more stable total returns and materially lower downside risk than non-core strategies.

A prime example was the GFC, where many non-core strategies resulted in permanent loss of capital. In contrast, institutional grade core property proved significantly more resilient, where it subsequently recovered and performed strongly.

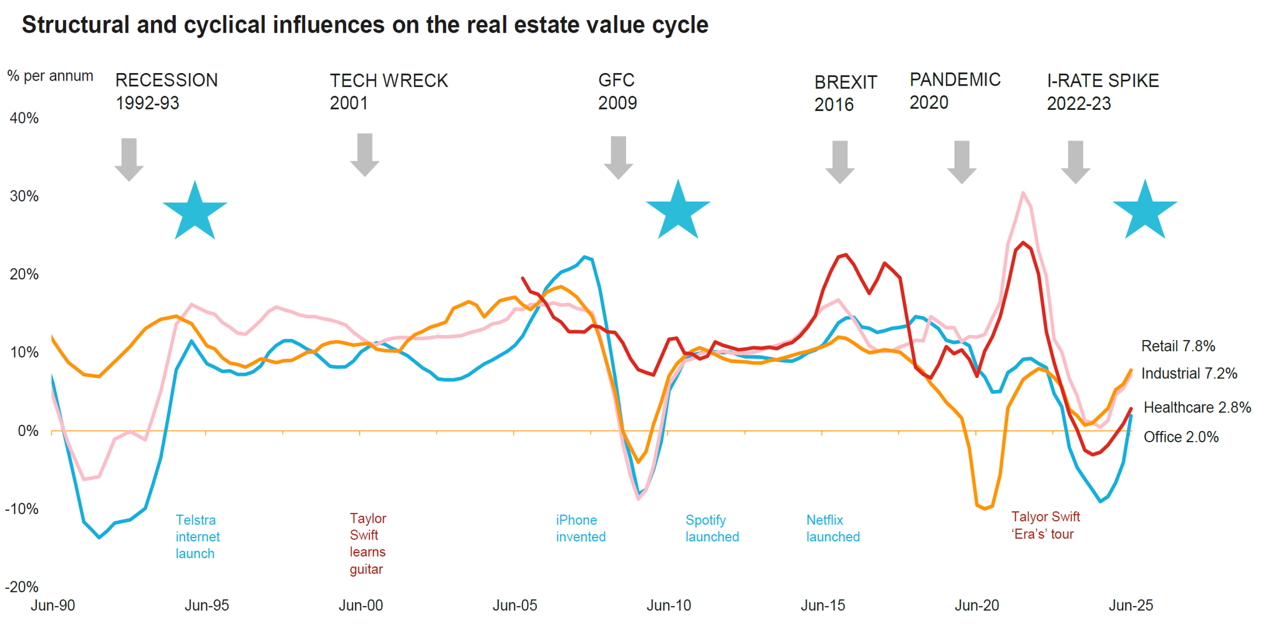

2026: The third great property cycle?

Approximately every 15 years the stars align for investing in Australian core property, where total returns exceeded 10% per annum for 5+ years.

Source: Dexus research using MSCI data with highlights added by PanGen

The first ‘strong-buy’ entry point occurred around 1995 following the ‘recession we had to have.’

The second ‘strong-buy’ occurred around 2010 post the GFC, in a period of stable economic growth and reducing interest rates and bond yields.

2026 is arguably the third ‘strong-buy’ point. Over the past 5 years, sharply rising interest rates and pandemic impacts have resulted in a significant downward pricing of Australian commercial property.

Despite inflation concerns, the Australian economy is strong, employment levels are high and population growth is solid.

And, importantly, there is a significant looming supply shortfall given the high cost of construction & development. For tenants seeking high-quality space, “TINA” applies – there is no alternative.

We believe these mega factors will continue to drive sustained above-average rental growth across all high-quality core real estate sectors for the foreseeable future.

Sector performance and outlook

Retail: Essential & experiential, with long term embedded upside

Our favoured retail property sector is high-quality, dominant and highly productive shopping centres. Effectively fully occupied, these malls continue to benefit from strong space demand as retailers look to secure space, especially given the low supply outlook. Additionally, these properties are strategically located in population centres with strong transport links, and as such many enjoy embedded upside potential via expansion of traditional retail space along with more diverse uses such as healthcare, office and living. We also like well-located convenience and large format retail properties, particularly with strong catchment growth and manageable competition.

Office: Quality & location matters

Office is a more cyclical sector and can present significant opportunities (and risks) at different periods. With ‘flight to quality’ a major theme, we favour Sydney and Brisbane CBD prime grade office towers located in gateway locations such as Sydney’s Circular Quay financial district and Brisbane’s ‘golden’ triangle. These properties are likely to continue to deliver above-average rental growth in the short to medium-term underpinned by robust tenant demand and supply to remain constrained, given assets value are typically significantly below replacement cost (in some cases 30%+).

Industrial: Strong fundamentals for the right assets

The industrial/logistics property sector has enjoyed a ‘super cycle’ of above-trend rental growth over the 10+ years, which is now moderating to more normal levels. As tenants look to enhance efficiencies, they will increasingly favour well-located, high-quality logistics & industrial properties with strong transport linkages close to population centres. We favour properties with these characteristics and believe these assets will continue to benefit from solid tenant demand, and some enjoy embedded ‘adjacent’ opportunities, such as data centres, increased densification and urban renewal.

Institutional grade ‘core’ property – now in the Goldilocks zone?

We believe that for the foreseeable future Australian prime-grade ‘core’ commercial real estate is set to deliver strong, above-average rental growth with strong fundamentals underpinned by a highly constrained supply outlook and strong tenant demand for prime grade properties.

With property values having ‘reset’ to attractive levels, we believe that core property offers a highly attractive risk adjusted return prospects, both on an absolute basis and relative to major asset classes such as equities, fixed interest, infrastructure, private credit and cash. What’s more, this asset class can enhance portfolio diversification.

Along with increasing transactional evidence and many institutional investors now underweight, we believe that now is the Australian core property ‘Goldilocks’ zone.

About the author

Ryan Bass is the founder and Managing Director of PanGen Capital, the Investment Manager, and is the lead portfolio manager. With over 25 years real estate investment management experience spanning unlisted and listed property markets, Ryan has built a strong track record of investment and funds management, including overseeing institutional unlisted pooled property funds, managing an active AREIT portfolio and an unlisted property fund, executing transactions, and serving on investor committees. Ryan’s expertise includes investment portfolio & funds management, equity raising, transactions, corporate actions, M&A, investor relations, fund documentation, reporting, financial modelling & analysis, compliance and marketing.

About the PanGen Australian Real Estate Fund

The PanGen Australian Real Estate Fund (PAREF) provides wholesale investors with access to institutional-grade 'blue-chip' Australian core real estate strategies typically available only to large superannuation funds and institutional capital—delivered through a highly efficient, private‑markets focused structure.

Important Disclaimer (Author) – For Wholesale Investors Only

PanGen Capital Pty Ltd (AR No. 1313733) and Ryan Bass (AR No. 1313763) are Authorised Representatives of Orsaro Capital Pty Ltd (AFSL No. 524448).

This document is intended solely for wholesale clients as defined under section 761G of the Corporations Act 2001 (Cth). It is provided for informational purposes only and does not constitute financial product advice, legal advice, or a recommendation to acquire or dispose of any financial product or service.

This material does not constitute an offer or solicitation to the public and is not intended for distribution to, or use by, retail clients. Any statements about performance, returns, or strategy are illustrative only and are not guaranteed. Past performance is not a reliable indicator of future performance.

This document is confidential and must not be copied, distributed, or reproduced without the prior written consent of the issuer.

Disclaimer(Kings Gate Capital Partners)

This article is authored and provided by PanGen Capital Pty Ltd (AR No. 1313733) and Ryan Bass (AR No. 1313763) who are Authorised Representatives of Orsaro Capital Pty Ltd (AFSL No. 524448). It is intended for wholesale investors as defined under the Corporations Act 2001 (Cth) and is not intended for retail investors.

The views expressed in this article are those of the author and do not necessarily reflect the official policy or position of Kings Gate Capital Partners. Kings Gate Capital Partners does not endorse this article or make any representation as to its accuracy. Any reliance you place on such information is therefore strictly at your own risk. You should consider the disclosure documents and seek professional advice before making a decision about any financial product.

For more detailed information contact us directly.